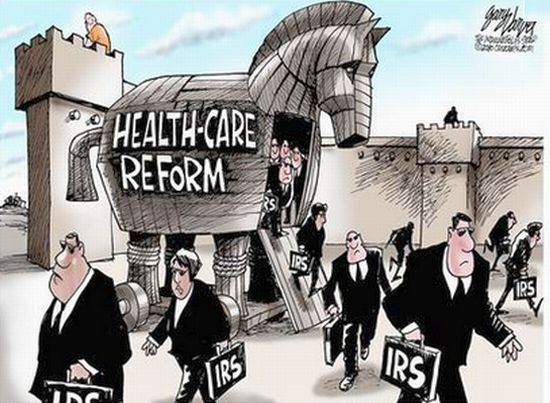

A case about to be decided by the U.S. Court of Appeals for the D.C. Circuit could stop Obamacare dead in its tracks in 34 states. Halbig v. Burwell is based on an illegal action taken by the Internal Revenue Service in 2012. Below I will outline that illegal action and the two sections of the PPACA (Obamacare) that are relevant in this case.

State-based exchanges and federally facilitated exchanges

Section 1311 of the PPACA describes state-based health insurance exchanges. That section outlines the powers granted to the IRS to provide APTC – “Advance Premium Tax Credits” (a.k.a. ‘subsidies’) that will be used to artificially lower the high cost of health insurance offered in a state-based exchange. Tied to those APTC’s is also the power granted to the IRS to levy a $2,000 or $3,000 excise tax (non-tax deductible) on all employers with 50 or more full-time employees (first 30 employees waived) if they do not provide PPACA approved health insurance. This is a lot of new power granted to the IRS and this is the primary reason the IRS is hiring thousands of new agents.

Section 1321 of the PPACA describes federally-facilitated exchanges and state-federal partnership exchanges – like the exchange the state of Illinois has chosen to establish. In these types of exchanges, the IRS is granted no authority to provide APTC’s or to levy excise taxes on any employer in that state for not providing PPACA approved health insurance. Since the crafters of the PPACA assumed that every state would willingly establish a state-based exchange, there was no money appropriated for federally-facilitated exchanges.

Thus far 34 states have chosen not to open a state-based health insurance exchange. As such federally-facilitated exchanges have been implemented in those states regardless of the wishes of those state’s legislatures.

The illegal action taken by the IRS

Here’s the kicker, in order to ‘fix’ this legal ‘opt out’ that section 1321 provides to states that choose not to open a state-based exchange. The Internal Revenue Service finalized a proposed rule on the 2 year anniversary of the passage of the PPACA that offers APTC’s -Advance Premium Tax Credits – through exchanges “established under section 1311 OR 1321 of the PPACA. Those six characters—”or 1321?—constitute as Cato’s Michael Cannon correctly describes “an unconstitutional and as such illegal rewriting of the statute.” By issuing tax credits where Congress did not authorize them, this rule triggers billlions of dollars in taxpayer provided “subsidies” and imposes excise taxes on employers with 50 or more full-time employees in all 50 states. Whether they have a state-based, state-federal partnership or federally facilitated exchange. Since the IRS is not a Legislative branch, this action was illegal. It was not authorized by Congress and as such it should not stand.

Worse yet, President Obama is following this new proposed rule as if it was codified law. This illegal action taken by the IRS and President Obama’s support of it is the crux of the Halbig v. Burwell case. If the U.S. Court of Appeals upholds the rule of law in this case it will mean the end of Obamacare in 34 states. In turn, it may be the final death blow to an unconstitutional and wildy unpopular law.

[…] C. Steven Tucker – Gulag Bound – TruthAboutObamacare.com – h/t to the NoisyRoom – Cross-Posted […]